The world of retirement savings can be confusing. Which option is best to help you move towards your goals? What is the difference between all of the retirement savings options? Over the next few weeks, we try to clear the muddy waters and help you gain an understanding of what retirement savings plan might be best for you.

The world of retirement savings can be confusing. Which option is best to help you move towards your goals? What is the difference between all of the retirement savings options? Over the next few weeks, we try to clear the muddy waters and help you gain an understanding of what retirement savings plan might be best for you.

Today we start with IRAs…

IRAs, Individual Retirement Accounts, are popular tools to save for retirement. The type of IRA you select can affect your long-term savings. It’s important to understand the various types of accounts to select the best one for you.

The main difference in Traditional and Roth IRAs comes down to when you pay income taxes. For Traditional IRAs, you pay taxes when you withdraw money in retirement. With a Roth IRA, you pay taxes on the front end, but no taxes when you withdraw.

Let’s start by looking at a Traditional IRA…

Contributions made to a Traditional IRA are tax-deferred. Taxes aren’t paid until you withdraw from the account at retirement. Contributions are tax deductible on both state and federal returns for the year you make the contribution in most, but not all, cases.

You can continue to contribute to a Traditional IRA until the age of 70 ½ as long as you have taxable income. Once you hit age 70 ½ you are required to make minimum withdrawals. Withdrawals will be taxed at current income tax rates.

Traditional IRAs do not have income limits like Roth IRAs do, but the amount you are able to deduct on taxes will be affected by your income and amount you are contributing to an employer plan. In general, if you expect to be in a lower income bracket when you retire, a Traditional IRA may be a good choice for you.

Now let’s look at the Roth IRA…

Contributions to Roth IRAs are after tax. Therefore, when you withdraw from a Roth IRA, you do not pay taxes.

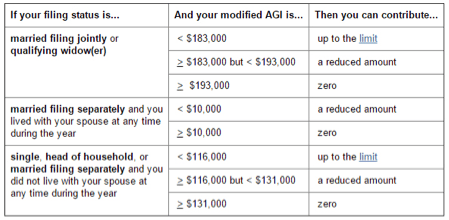

With a Roth IRA, you can continue to contribute as long as you have taxable income (even after age 70 ½). However, the contribution limits to Roth IRAs are sometimes hard to understand.

Here’s the calculation chart provided by the IRS:

*The IRA contribution limit for 2015 and 2016 is $5,500 ($6,500 if you’re age 50 or older), or your taxable compensation for the year, if your compensation was less than this dollar limit. This limit does not apply to rollover contributions and qualified reservist repayments.

(source)

In general, Roth IRAs are recommended for those who expect to be in a higher income bracket when they retire than they are in today. It is usually better to pay a smaller percentage of taxes on your income now rather than paying a larger percentage of taxes on your income later. But, your income may disqualify you from taking advantage of a Roth IRA, and a Traditional IRA may be a better choice.

We suggest working through your retirement decisions and IRA contributions with a financial planner to help make the best decision for your investments while making sure IRS guidelines are honored.

If you are interested in a complimentary consultation, give us a call today at 303.639.5100 or visit shwj.com.

*Research for this post done on IRS.gov